This blog will follow on topics that have been previously summarized in the following New Age Metals blogs and will explore a common measuring stick for mineral property value – the Lassonde Curve:

Everything that we see around us is made from something that is either farmed or mined. There are so many critical materials that are mined across the world that go into technologies, infrastructure and other end products that are integral components of our society. If you were to scan the globe you would find many producing mines and many more properties that may or may never become a mine. Behind each of these mines or properties is a story and a company made of industry experts in geology, finance, mining, and more – in the case of the properties, not all of them succeed. Taking a prospective mineral property from acquisition and discovery of a mineral resource all the way through to production is a losers game. For those that have the fortitude – and sometimes a bit of luck to come across a property that ends up becoming a mine, the process can be life-changing. Investors in the mining space look for opportunities to form a position in a company at the ground level and put faith in management teams to deliver results and create value for shareholders as they progress through the mining lifecycle.

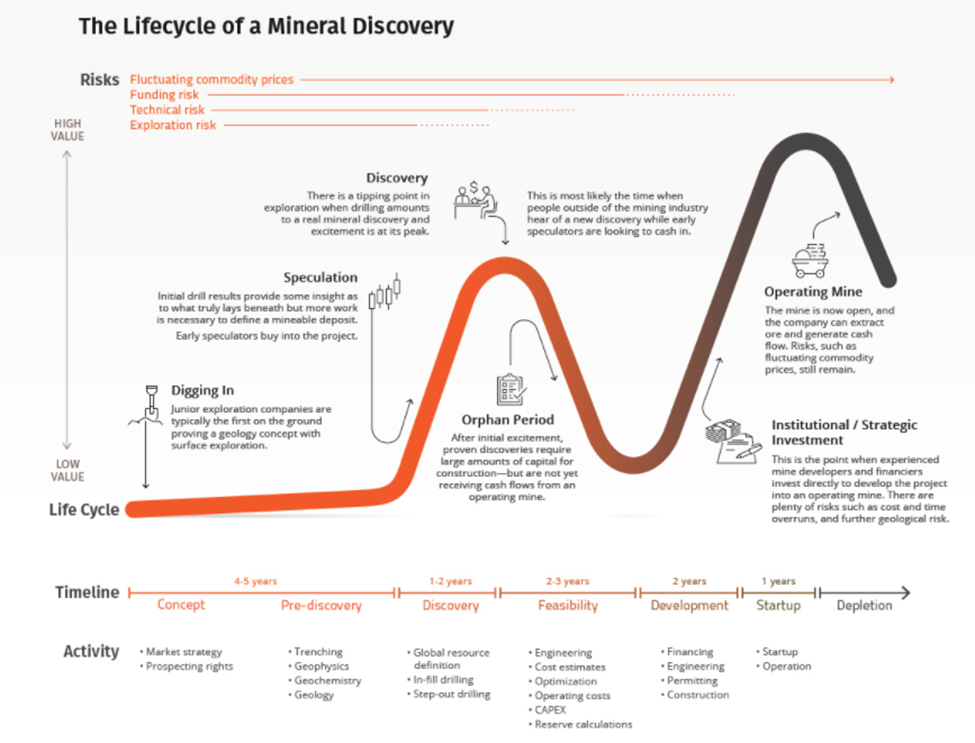

Pierre Lassonde, member of the Canadian Mining Hall of Fame and one of the founders of Franco-Nevada, the largest gold royalty company on the planet, put together an illustration of the intrinsic value of a mineral property over its life from beginning to end. This illustration is now referred to as the Lassonde Curve and should serve as a guide to any investor who is focused on early-stage opportunities (junior mining companies focused on exploration and development of mineral properties).

Junior mining management teams can very clearly speak to the trends suggested in the Lassonde Curve and can use the idea of the Lassonde curve to communicate to investors how their upcoming corporate milestones may impact the intrinsic value of the company.

Users of the curve may debate on the real value drivers that they perceive to affect the stock price, however, generally speaking, the curve does communicate the story well. Some versions of the Lassonde Curve, like the one above show an approximate timeline for companies progressing a property through the various stages, however, there are so many risk factors at play for a mining company that can result in shrinking or expanding these timelines drastically. If it were as easy as following suggested timelines on a curve, investing in mining would be a whole lot easier for the generalist investor.

It will be useful to provide some more background on each of the suggested phases of the mining life cycle included in the Lassonde Curve.

Concept

The first step involves acquiring a prospective mineral property. Without the property we have nothing to explore, drill, develop and advance towards production. The decision to acquire a prospective property is likely guided by previous surface or airborne exploration work that has either mapped out potential mineral occurrences or mineral prospectors have collected rock samples from a property and confirmed the thesis about the presence of value materials from a third-party analysis by a metals / minerals laboratory. After a company can tell the market that they own a prospective property, it is their responsibility to communicate the property’s value proposition to the capital markets who may in return, invest their capital into a property to test whether or not a metal deposit may exist. The process of securing the financing to complete mineral exploration work is easier said than done. With cash in hand, a junior miner can complete numerous analyses depending on the type of mineral deposit that they are hoping to discover. This work is likely conducted by a team of geologists and could include trenching, geophysical surveying and more. All of this work is meant to support a decision to explore for below surface extensions of mineralization, via what some industry people call the truth machine, a diamond drill. New Age Metals was in the concept stage with its flagship River Valley Palladium Project in 1999, when the company’s management team reviewed available data from three individual prospectors who owned land tenements that were prospective for Platinum Group Metals only 100 kms from Sudbury. A decision was made to acquire these land tenements based on encouraging geological data held by the prospectors. New Age is in the concept phase and starting down the track of a discovery in Manitoba at its portfolio of hard rock lithium properties.

Discovery

After a company has proven a concept of a potential mineral deposit, diamond drilling can tell you the extent to which the minerals exist below the surface. Diamond drilling programs are capital intensive, however, they can be extremely rewarding. A drill core containing sufficient amounts of metals will encourage additional exploration. There is no exact definition of what a discovery is, but we can view it as the identification of a significant amount of metals below the surface on a prospective property. New Age Metals made a PGM discovery at River Valley in April 1999. The discovery stage is usually a part of the Lassonde Curve where company valuations can really grow. As more work continues to hopefully discover more metal, investors may start to take more notice of a junior mining story based on what they know about the general trend of a discovery as depicted by the Lassonde Curve. Strategic decisions are made by management teams to either continue to drill and expand mineral resources or perhaps at the same time, make the decision to communicate to the market the size of the resource via a Mineral Resource Estimate (MRE) Technical Report. An MRE report will take exploration drilling data and geologists and engineers will model that information using advanced software packages to output a statement of the Mineral Resources at a property. The table below is an excerpt from New Age Metal’s latest MRE from 2021:

Notes*:

1. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability

2. The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues

3. The Inferred Mineral Resource in this estimate has a lower level of confidence than that applied to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of the Inferred Mineral Resource could potentially be upgraded to an Indicated Mineral Resource with continued exploration

4. The Mineral Resources were estimated in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), CIM Standards on Mineral Resources and Reserves, Definitions (2014) and Best Practices Guidelines (2019) prepared by the CIM Standing Committee on Reserve Definitions and adopted by the CIM Council. Numbers may not add exactly due to rounding

5. The Mineral Resource Estimate is based on US$ metal prices of $1,850/oz Pd, $900/oz Pt, $1,600/oz Au, $3.00/lb Cu, $16/lb Co, $6.50/lb Ni, $8,000/oz Rh, $18.50/oz Ag. The US$:CDN$ exchange rate used was 0.75.

6. The NSR estimates use flotation recoveries of 80% for Pd, 80% for Pt, 80% for Au, 85% for Cu, 25% for Co, 90% for Ni, 80% for Rh and 65% for Ag and smelter payables of 80% for Pd, 80% for Pt, 85% for Au, 85% for Cu, 50% for Co, 90% for Ni, 80% for Rh and 65% for Ag.

7. The pit optimization used a mining cost of $2.25/t mined, combined processing and G&A costs of CDN$15/t, and pit slopes of 50º. The out-of-pit Mineral Resources used underground mining, processing and G&A cost of CDN$50/t.

8. See Company press release dated October 5, 2021. More details, including the NSR (Net Smelter Return) formula, are available on NAM’s website (www.newagemetals.com) and under the Company’s profile on SEDAR.

*Qualified Person

The contents contained herein that relate to the scientific and exploration results for the River Valley Project are based on information compiled, reviewed or prepared by Dr. Bill Stone, P.Geo., a consulting geoscientist for New Age Metals. Dr. Stone is the Qualified Person as defined by National Instrument 43-101 and has reviewed and approved the technical content of this document.

Feasibility

After delineating a mineral resource through diamond drilling, junior miners may elect to move into the engineering or feasibility phase of the Lassonde Curve. This phase of the mining life cycle usually requires more capital than the discovery phase. It is in the engineering phase where engineers from a variety of disciplines come together to evaluate the feasibility of a mining operation at a property. There are various levels of engineering studies that effectively build on each preceding study to analyze a property with a higher degree of precision. Investors in junior miners should know the different types of studies and what they mean for the property in question. New Age Metals completed its first engineering study at its flagship River Valley Palladium Project in 2019. This was a Preliminary Economic Assessment (PEA). PEAs are largely desktop analyses and so they are conceptual in nature. They will integrate the previous exploration and mineral resource data into a study that develops a preliminary mine plan and wraps a financial analysis around the mining and processing plan to output financial metrics used to evaluate the project as an investment opportunity. The Feasibility phase is often one where market speculators are not interested due to the study timelines and nature of the work that does not produce consistent news flow that captures market attention. A positive study, when announced, can certainly act as a major catalyst for a company; however, the time between announcing a study and publishing its results is often referred to as the orphan segment of the Feasibility phase on the Lassonde Curve. New Age Metals is currently advancing River Valley through a Pre-Feasibility Study (PFS) which is slated to be completed in the second half of 2022. The PFS is a more advanced engineering study compared to a PEA and involves more site plan engineering work to ascertain whether the proposed locations of site infrastructure from the PEA actually make sense in practice.

Development

After discovering a mineral deposit and de-risking it through rigorous engineering and financial studies, companies may be able to develop the property into a real mining operation. Thinking back to the start of this blog, we stated that only a small number of prospective mineral properties become mines. That is to say, that most of the properties around the world never reach the development phase on the Lassonde Curve. It is common to see management teams transition at the development phase. More often than not, the team that discovers and derisks a property is not the same team to develop and operate the mine. These skill sets are very unique and they can be thought of as being mutually exclusive in many cases. Additionally, development is not cheap. As the property moves along the Lassonde Curve, it usually requires more capital to continue its trajectory and path towards production. If a management team can secure the proper funding and permits for their project to make a construction decision, investors have another chance at a major share price movement similar to share price behaviour after a discovery is made. This is a signal to investors that the company or project can transition from a site that takes funds, to a mining operation that produces revenues for the operator. A major source of value creation for a company in any industry, is when real, tangible data in terms of finances are available to investors to help them form their own investment decisions.

Startup

Investors who have held their investment until this point can pat themselves on the back—this is a rare moment for a mineral discovery. The company is now operating a producing asset which is in turn, generating revenues. This is a major transition for a mineral company. At the startup or production phase, some of the early speculators that had positions in the stock may look to exit their positions, however, this is not always the case. The capital markets can now evaluate the operating, ESG, and financial performance of the company to make their own investment decisions.

The Lassonde Curve is a concept that any junior mining speculator / investor should learn about and use it to help form their expectations for the timing and potential upside of their investment in the junior mining space depending on the phase of the mining life cycle a mineral project is at. We hope that connecting the New Age Metals projects to their respective phases of the curve is helpful for readers. Although the Lassonde Curve is a solid guideline, there are many other factors at play that can influence the intrinsic value of a junior miner’s share price and anyone involved in the space must have that awareness of the potential volatility of this business.