The junior mining sector is known for its cyclicality, with periods of exuberance followed by valleys of stagnation. As we enter 2025, several converging factors suggest that we are on the brink of an up-cycle for junior mining stocks. From increasing commodity prices to geopolitical dynamics and historical trends, the stars appear to be aligning for this sector to thrive once again.

Historical Cyclicality of Junior Mining Stocks

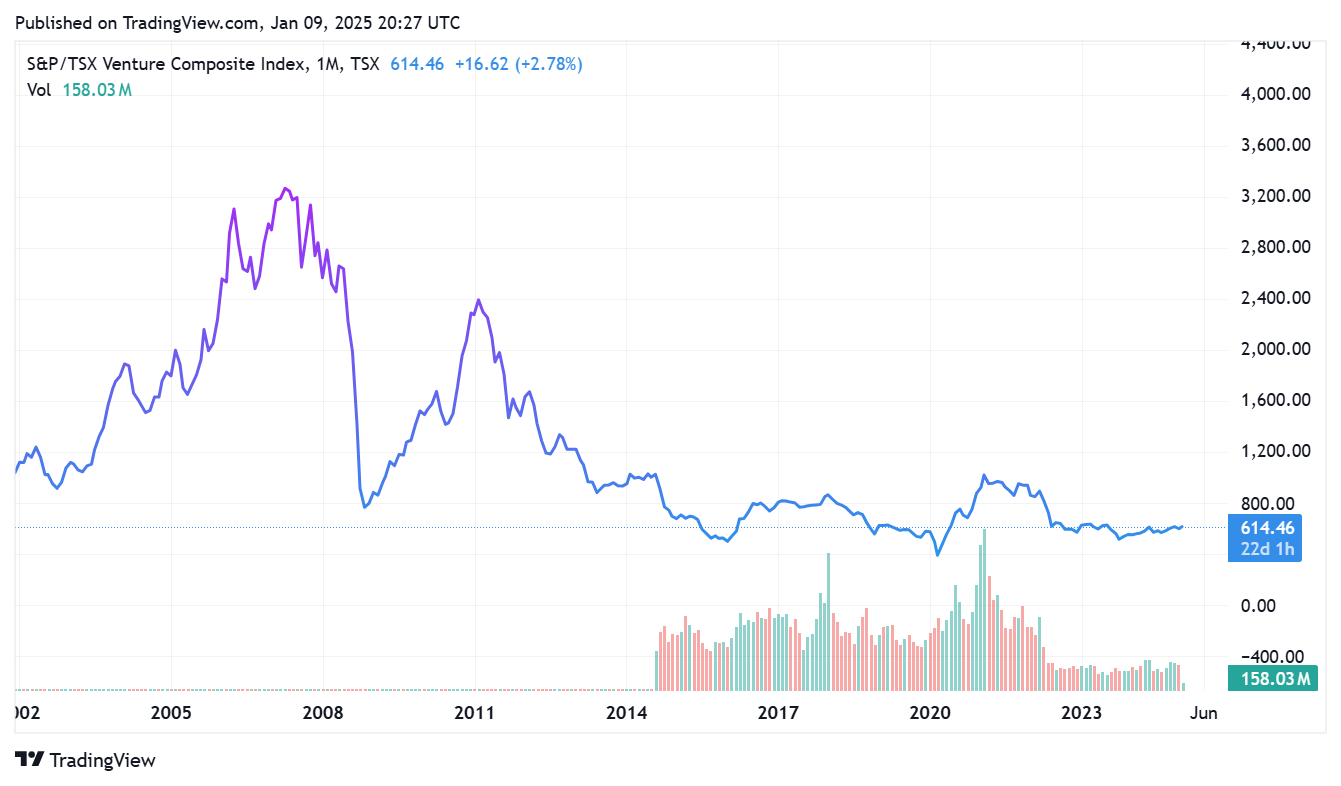

Junior mining stocks are notoriously cyclical, often reflecting broader macroeconomic trends and commodity prices. Over the past few decades, we’ve observed clear periods of bullishness in the sector, typically lasting 3–5 years, driven by surging metal prices, increased exploration budgets, and investor sentiment. Historically, these cycles are separated by 3–5 years of dormancy, where valuations stagnate and capital inflows slow.

By analyzing past cycles, we are due for a new wave of bullish momentum. The last significant boom occurred in the late 2010s, fueled by rising gold and battery metal prices. With a mix of favorable market conditions now brewing, 2025 could mark the beginning of the next significant up-cycle.

The Toronto Venture Composite Index From 2020 to 2025. Prices have come down from their highs in 2021. It is possible we may enter a new up cycle stage in the near future.

Our last big cycle began in the later part of 2002 and peaked in 2007. Are the junior markets poised for another super cycle?

Rising Gold and Silver Prices: A Beacon for Junior Miners

Gold, the perennial safe haven, has experienced a strong resurgence due to persistent economic uncertainties, inflation fears, and declining trust in fiat currencies. Prices recently breached the $2,000/oz mark and show no signs of slowing down. For junior mining companies, this is crucial—higher gold prices make exploration projects more economically viable, attract new investors, and lead to increased funding opportunities.

The recent uptick in mergers and acquisitions within the gold mining sector is also indicative of a broader bullish trend. Majors are increasingly looking at juniors to replenish their reserves, setting the stage for outsized gains in junior gold stocks.

Uranium: A New Energy Renaissance

Uranium is another commodity experiencing a renaissance. With the global pivot toward cleaner energy and the revival of nuclear power as a sustainable energy source, demand for uranium is skyrocketing. Prices have surged past $70/lb, their highest in over a decade, as governments and private enterprises prioritize energy security.

Junior uranium explorers are uniquely positioned to benefit from this trend. Many of these companies operate in regions like Canada’s Athabasca Basin and Kazakhstan, where uranium resources are plentiful. Increased demand, coupled with dwindling reserves at older mines, places these juniors at the forefront of the next energy revolution.

Copper: The Backbone of Electrification

The green energy transition hinges on copper. From EV manufacturing to renewable energy infrastructure, copper demand is poised to grow exponentially. Prices have remained robust, hovering near $4.00/lb, as supply deficits loom on the horizon. This is especially critical for juniors, as copper exploration projects, often overlooked during bear markets, are now back in the spotlight.

Emerging economies like China and India, combined with North America’s infrastructure push, further underline the importance of copper. Juniors exploring in stable jurisdictions with high-grade copper deposits could see massive appreciation in value as supply shortages become more acute.

Antimony and Palladium: Critical Metals for a Changing World

Antimony, a lesser-known critical metal, is gaining attention due to its applications in flame retardants, batteries, and military uses. With China dominating global production, securing alternative sources has become a priority for Western countries. Junior miners with antimony projects are positioned to fill this gap, creating a niche opportunity in the critical metals space.

Similarly, palladium is poised for a price rebound. Used predominantly in catalytic converters and increasingly relevant in hydrogen fuel cells, palladium demand remains strong. Russia, the world’s largest palladium producer, faces supply-side constraints as its reserves dwindle and geopolitical pressures mount. Juniors with palladium exposure, like those exploring in Canada, could benefit from the anticipated price increases.

Russia’s Supply-Side Constraints: A Boon for Western Miners

Russia’s dominance in global supply chains for metals like palladium and antimony has waned due to dwindling reserves and sanctions. These pressures have created a void that Western junior miners can fill. Companies exploring in geopolitically stable regions like Canada, the United States, and Australia have a unique advantage as buyers seek reliable and ethical sources of critical materials.

This dynamic is particularly pronounced in palladium and uranium markets, where Russian supply disruptions have triggered price spikes. The shift underscores the importance of investing in juniors with projects outside of geopolitically volatile regions.

China’s Dominance of the Critical Metals

China’s control over the global supply of critical metals, including rare earth elements and lithium, has sparked a push in North America and Europe to develop independent supply chains. This shift is creating a bullish outlook for the industry as governments and private investors prioritize domestic exploration and production to reduce reliance on China. These efforts are further supported by policies promoting ESG-compliant practices, technological advancements, and subsidies for critical metal projects.

As demand for local and sustainable resources grows, companies in North America stand to benefit from higher prices and increased investment, showcasing this as an opportune time for growth in the sector.

Why Now?

- Improved Investor Sentiment: Rising prices across multiple commodities have reignited interest in junior mining stocks, drawing both retail and institutional investors back to the sector.

- Supply Chain Challenges: Dwindling reserves at major mines and geopolitical disruptions have placed juniors in a unique position to fill the supply gap.

- Renewed Exploration Budgets: Higher commodity prices enable juniors to secure funding for exploration, driving growth and discoveries.

- Macro Trends Favoring Metals: The green energy transition, nuclear power resurgence, and infrastructure spending underscore the long-term demand for metals like copper, uranium, and palladium.

Conclusion

The junior mining sector is primed for a significant up-cycle, supported by rising commodity prices, historical trends, and shifting geopolitical dynamics. From gold and uranium to copper, antimony, and palladium, the demand for key resources places juniors at the forefront of the next mining boom. For investors, this is a time to position strategically in the sector, leveraging its cyclicality to capture outsized gains.

New Age Metals has a critical metals portfolio of lithium exploration stage projects and a development stage palladium project. Management’s 2025 mandate is to aggressively acquire additional critical metals projects to add to its portfolio. The Company is looking to capitalize on the need for North America to secure domestic supply chains of minerals like copper, PGMs, antimony, uranium and others.

As history shows, junior mining stocks don’t stay dormant for long. New Age Metals is well positioned with a tight capital structure, a healthy treasury and an aggressive experienced board of directors and management team.